New Solutions For Revitalizing Big Pharma R&D

by Jenny Hsu, Ph.D. | June 18, 2018

An unsustainable ecosystem

Drug research and development (R&D) lies at the heart of the pharma industry and receives a considerable allocation of its resources. Over the last decade, R&D spending across U.S. pharmaceutical companies has increased from $25 billion to $59 billion. The Tufts Center for the Study of Drug Development estimates the average R&D cost of a new drug to be a controversial $2.9 billion.

Unfortunately, the return on these large investments seldom satisfies. The number of drugs receiving FDA approval remains small and unchanged, and only 2 out of 10 approved drugs return revenues that match R&D costs. Meanwhile, blockbuster drugs representing an overall $17 billion in sales are set to lose patent protection in 2018. Faced with criticism on its spending tactics and competition from generics, pharma companies are seeking strategies to transform the unsustainable R&D ecosystem. In January 2018, the pharma industry announced an unusual $39 billion in planned mergers and acquisitions (M&A), spurred in part by new laws that reduce the tax on bringing offshore cash into the country. These developments, along with the emergence of new R&D models, suggest that the industry must carefully consider partnerships that can boost pipelines and repair inefficiencies in the R&D process.

Fixing the R&D chain, link by link

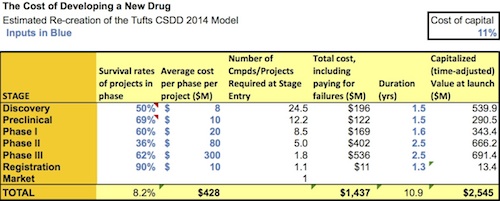

Drug R&D consists of four major steps: discovery, preclinical, clinical, and FDA review and registration. The discovery and preclinical stages are sometimes grouped together as the “R” of “R&D,” while the clinical stage can be thought of as the “D” of “R&D.” A graph by a life sciences expert and venture capitalist breaks down R&D costs across these steps. While the graph does not account for the fact that some drugs cost more or less to bring to market depending on the disease area, these estimates are largely accurate. They reveal that the high cost of R&D comes not only from out-of-pocket costs, but long timelines that could be dedicated to a more fruitful project, and high rates of failure for a large number of drug candidates. Revamping R&D, experts conclude, will require targeting every step of the process.

{kind=link}

The “R” of “R&D” – discovery and preclinical

During the discovery and preclinical phases of R&D, researchers study the mechanisms behind a disease, test thousands of drug candidates on non-human models, gather information on toxicity and dosage, and ensure that the best drug candidates can be tested on humans. Discovery costs an average of $196 million over 1.5 years, while preclinical testing costs $122 million over 1.5 years. While not inherently as expensive as clinical trials, these phases come with a high opportunity cost: on average, only 1 in 5000 drug candidates that reach the pre-clinical phase survives clinical trials to become an approved drug. These statistics suggest that millions may be spent on expensive clinical trials without payoff, unless strategies are in place to predict whether a drug will actually perform as expected in a patient.

On this front, Morgan Stanley predicts continued “technology convergence,” in which non-tech companies buy technology firms to make their R&D more efficient. Incorporating tech into their pipelines is estimated to generate up to $100 billion in value annually across the U.S. healthcare system. It can also help pharma companies break into markets for precision medicine, which are relatively small compared to those for blockbuster drugs, yet appealing given the looming patent cliffs.

As of April 2018, at least 18 pharma companies and 75 startups are applying machine learning to drug testing. San Francisco-based Atomwise tests more than 10 million drug simulations every day for their potential efficacy and side effects. It was named as a favorite by consulting company CB insights and has over 40 clients in biotech and academia. TwoXAR in Palo Alto, which recently raised $10 million in funding, has a similar computational platform for drug testing, and also works with clients to validate drug candidates in preclinical studies in the lab.

In addition, semantics technologies have become critical for finding correlations in the literature between disease pathologies and drug targets, given that 2.5 million scientific papers are published every year. This approach has already revealed, for example, that only 60% of “druggable” targets have been targeted by pharma companies. BenevolentAI is a leader in this field, recently raising $115 million in funding and working on 20 drug R&D programs. Exscientia, the first company to apply artificial intelligence to drug R&D, combines semantics technologies with computational drug testing for a fully automated service.

PricewaterhouseCoopers also states that in order to improve R&D, big pharma will need to learn more about human biology. This need has led pharma companies to seek more collaborations with academic institutions (full list here). The leaders in this model are AstraZeneca, Johnson & Johnson, and GSK, who respectively had 18, 15, and 13 academic partnerships in 2014.

Pharma companies use different strategies to divert academic research towards drug discovery. GSK’s Discovery Fast-Track Program sends out an open call for proposals every year, the most successful of which receive funding. Alternatively, Johnson & Johnson’s J-LABS, located in San Francisco and other cities across the globe, is an example of a long-term “hub” with academia that provides lab space and access to industry resources. However, experts caution that academic partnerships can only flourish if their members can establish how profits will flow. In the successful model of the TB Alliance, academic institutions collaborate with pharma on drugs against infectious diseases, while receiving funding from the government and other public organizations. Pharma companies can enter a disease space where drug costs must remain low, and academics can continue to receive financial backing and incentives. This model has resulted in new drugs against malaria and meningitis A, and may prove fruitful for some disease spaces.

Many such partnerships operate on an open source model. Lack of information accounts for ~85% of the $200 billion spent on healthcare, as ~50% of data from drug development is never published for others to analyze and use. Under an open access system, such as the Structural Genomics Consortium, collaborators can propose projects for the group, but must share all their results and promise never to file patents.

A final alternative is crowdsourcing – offering awards to anyone who can propose an answer to an R&D problem. Eli Lilly was an early pioneer of this approach, launching Innocentive in 2001, which now exists as a third party that works with other pharma companies, and boasts 365,000 registered problem solvers. 2017 was the biggest year yet in terms of number of projects, and experts predict even more players in 2018.

The “D” of “R&D” – clinical trials

The “D” phase of “R&D” consists of Phase I, Phase II, and Phase III clinical trials designed to gauge the safety and efficacy of drugs on humans. It is estimated to cost an average of $1.1 billion over 6.6 years. During this phase, in addition to reimbursing the many personnel involved, drug companies must also grapple with the high cost of capital. This can come from the long process of choosing a study site, which increases the cost of a clinical trial by at least 20%, and from problems in recruiting patients, which delay 80% of clinical trials. Furthermore, experts estimate that 30% of patients later drop out of a trial, and that 85% of clinical trials fail due to patients dropping out.

Drug companies therefore rely increasingly on contract research organizations (CROs), which provide expertise in the form of contractual services. While nearly anything that pharma needs to do can be outsourced to CROs, CROs focusing on clinical trials dominate the market. The CRO market is predicted to grow from $30 billion in 2016 to $51.3 billion by 2024, due largely to renewed efforts at innovating clinical trials.

Big data analytics have emerged as essential for this process. Flatiron Health was an early leader in the field, linking multiple sources of healthcare data from cancer patients into a single repository to quickly determine eligibility for new oncology trials. It was acquired by Roche for $1.9 billion in early 2018. Machine learning can also be used to optimize different aspects of clinical trial design. For example, despite constant calls for reform, eligibility criteria grow more complex every year, shrinking the pool of candidates who can participate in a trial. Less than 2% of cancer patients are treated in clinical trials in part because of this problem. SF-based Datavant aims to find solutions by combing through the clinical trial results, pharmacy records, and genomic information of over 150 million people, and partnering with other big data analytics groups such as G3 and Verge to expand its repositories.

To recruit patients, CROs have shifted their focus away from physician referrals and towards digital campaigns, which are faster and friendlier and have greater reach. Clara Health and Seeker Health, both in the Bay Area, are developing social media campaigns to educate patients and assign them to their nearest clinical trial site. Their platforms also include patient-centric features, such as a search tool for finding clinical trials, support teams for managing travel and insurance, and a podcast for patient stories.

Additionally, by equipping patients with sensors and wearables, companies may be able to improve patient engagement and collect trial data without setting up as many clinical sites. In 2017, Sanofi teamed up with the CRO Parexel to test the impact of wearables on trial success and cost reduction. The results of the study will be published in the near future. Meanwhile, Oracle Health Sciences announced in April 2018 their new offering of a mobile health platform to streamline multiple sources of patient data. Consulting group Kaiser Associates predicts that 70% of clinical trials will utilize wearables by 2025.

Ultimately, the end goal is to make clinical trials fully remote, including sending drugs, wearables, and information in the mail. LA-based Science 37, which recently started an office in SF, boasts a platform that allows researchers to identify patients for clinical trials, and then communicates daily instructions to participants by mobile app. The startup also develops strategies to record clinical outcomes remotely. Visible symptoms can be captured in screenshots that are then emailed to a clinician for analysis, while a mobile nurse visits participants to collect samples for bloodwork.

The ripple effect of R&D reform

While these new R&D strategies are exciting, the primary concern is that few precedents have been set for them. Artificial intelligence in pharma, while outperforming human scientists, is still in its early stages. The first molecules designed by algorithms are just now being sent for testing in clinical trials. On the clinical end, the first attempt at remote trials was discontinued possibly because patients distrusted sending personal information online. But pharma companies are not helpless in optimizing these strategies. Steve Arlington, President of Pistoia Alliance, reports for Stat that big pharma must support the development of startups that work on R&D, instead of simply waiting to acquire them. This strategy lessens the disruptive effects of an acquisition on a smaller company, and can give startups a necessary leg up in building a business. Additionally, pharma companies are collaborating more with each other through networks such as TriNetX, which aims to innovate clinical trial design.

Meanwhile, the restructuring of R&D, in particular the increasing emphasis on technology, suggests that job-seekers looking to work in the biotech and pharma industries should expect new opportunities and demands. Nature Careers emphasizes that companies are hiring more data scientists to work on drug discovery, as well as web engineers, graphic designers, and other non-scientists to design the apps required for remote clinical trials. Academic institutions are also feeling the effects of R&D restructuring. Popular institutions for pharma deals from 2008 to 2013 were led by heavy hitters like Harvard, the Broad Institute, and UCSF. But more strong faculty are spreading themselves out across the nation, and top NIH-funded institutions include universities that have traditionally laid low on pharma’s priority list. In their hunt for innovation, pharma companies are eager to tap into these unexplored resources.

In addition, pharma companies are becoming a primary source of funding for academic research. Government funding began to flatline in 2012, and for the first time in decades, no longer supports the majority of basic research. Corporate funds now provide $3 to basic research for every $1 of government money. The appeal of corporate funding may mean that academic institutions must adapt to tighter project deadlines, as well as delays in publishing results until patents are filed. In addition, whether academic scientists are content with having their proposals funded, or whether creative solutions are proposed for sharing profits, remains to be seen. At the end of the day, big pharma is here to stay. How other industries are affected by R&D restructuring will be interesting to monitor in the next few years.

By: Jenny Hsu, Ph.D. is a Biotech Connection – Bay Area Science Communication Fellow

Have ideas for a BCBA article? Email bioconnect.bay@gmail.com